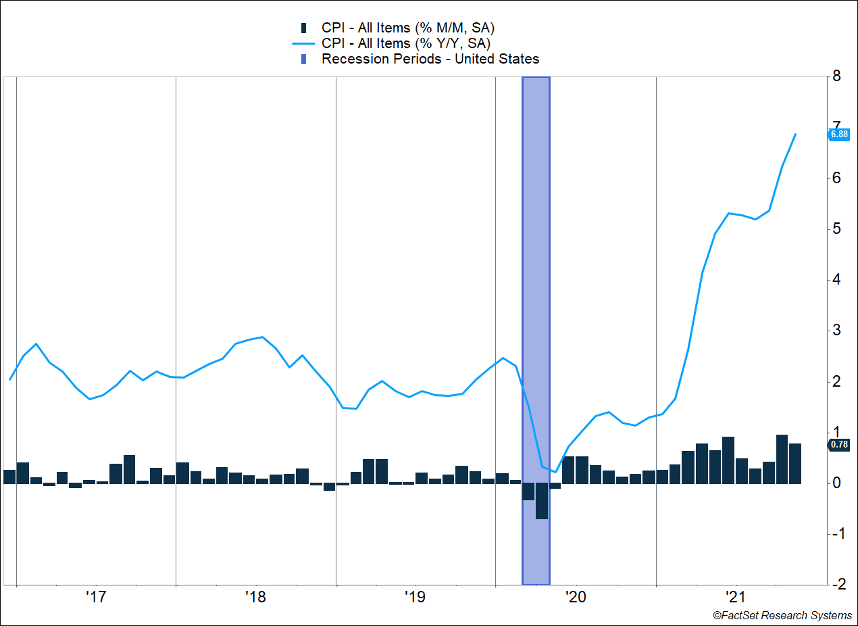

Consumer prices continued their rapid climb in the U.S. The Consumer Price Index surged 0.8% in November and is now 6.8% higher than one year ago. Big increases in food and energy prices accounted for nearly half the gains in the monthly and annual numbers. Core inflation, which excludes those more volatile elements, increased 0.5%. Even though the inflation rate was quite high, expectations for future inflation dropped slightly (Figure 1).

Key Points for the Week

- Food and energy price increases helped push the Consumer Price Index up 0.8% last month, and annual inflation rose to 6.8%.

- Job openings in the U.S. reversed the recent trend and increased to 11

million jobs available. - Chinese consumer prices have risen 2.3% in the last 12 months, spurred by higher vegetable prices.

Inflation is also affecting the job market, and the number of openings surged based on October’s data. The Job Openings and Labor Turnover Survey (JOLTS) indicated openings climbed back above 11 million. The quit rate slowed slightly from 3% to 2.8%. Chinese inflation remains lower than in the U.S., although government pressure is likely a factor in keeping prices contained.

Stock prices reacted positively to the week’s data. The S&P 500 index leapt 3.8% last week and closed at record levels. The MSCI ACWI soared 3.1%. The Bloomberg U.S. Aggregate Bond Index surrendered 0.7% as inflation pressure and concerns about higher rates pressured bonds. Bond prices move in the opposite direction of yields. The Federal Reserve’s meeting this week will be watched closely to determine if the Fed will taper its bond purchases more quickly and raise the possibility that interest rate increases could happen sooner than expected.

Figure 1

Prices Rise, Expectations Wane

U.S. consumer prices just keep climbing. The Consumer Price Index increased 0.8% last month and has risen 6.8% in the last 12 months. The 6.8% annual increase is the fastest rate since 1982, when inflation was falling from its peak during the Carter administration. Inflationary pressures are creating a challenging economic environment in which salaries have risen a rapid 4.8% but many workers are losing purchasing power because inflation is rising even more quickly than wages (Figure 1).

Core inflation is also increasing but at a more moderate pace. Food and energy price increases accounted for roughly half the jump in headline CPI last month. Removing those two segments led to a smaller increase for core inflation. Price hikes for reopening items increased last month. New and used vehicles, airline fares, hotels, and shelter costs all rose more than the 0.5% increase in the core index.

The inflation data once again impacted interest rates as the yield curve steepened last week. The 10-year Treasury increased 0.14%, and the two-year climbed 0.07%. This puts it close to where it was in early November before the market saw a spike in equity volatility, which temporarily drove money into the safety of U.S. Treasuries.

Even though inflation keeps climbing, expected inflation is beginning to decline. The five-year breakeven inflation rate serves as a barometer for future inflation expectations. It calculates the difference in yield between a five-year Treasury and a five-year inflation-protected bond. It peaked last month at 3.17% but has since retreated to 2.76% (Figure 2). This indicates the market still expects inflation to run above the Fed’s 2% target but not as far above as expected just a few months ago.

It may surprise some that inflation expectations are already falling even as the monthly data remains so strong. There are likely a few reasons for the seeming paradox. First, the 12-month rolling inflation comparisons are about to get more difficult. Inflation was very low this time last year. Starting early in 2021, inflation began to spike, and price hikes aren’t likely to continue at the same torrid pace. Leading indicators also show improvement in shipping data and other transportation logjams, which indicate the inflationary pressures from trade and goods shortages are slowly abating.

The Fed’s meeting this week will provide the next big-effect decision point around inflation. The Fed seems likely to increase the pace of tapering its bond purchases. Buying fewer bonds isn’t likely to reduce inflationary pressures. It isn’t clear how much tapering makes a difference, particularly in a pandemic. More importantly, accelerated tapering means the Fed will be done with its special purchases sooner than expected, and that may clear the way for higher interest rates in the future.

Figure 2

–

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

https://fred.stlouisfed.org/series/CPIAUCSL#0

https://www.bls.gov/news.release/cpi.nr0.htm

https://www.bls.gov/news.release/jolts.nr0.htm

https://www.reuters.com/markets/europe/chinas-factory-gate-inflation-slows-nov-2021-12-09/

Compliance Case #01211887