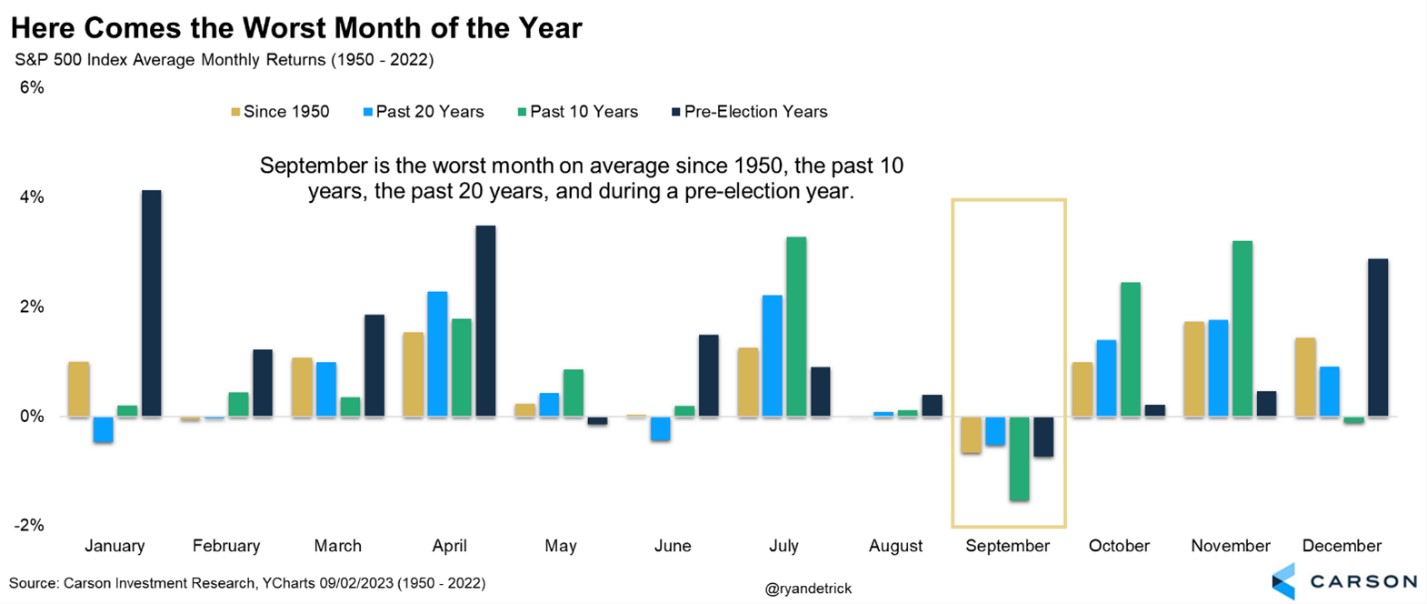

Stocks have had a rough start to September on the heels of an August slump. As we noted last week, this type of seasonal weakness is normal. The chart below shows that during various timeframes, August and September can be tricky. September, specifically, has been the worst month of the year looking back 10 years, 20 years, and since 1950. It has also been the worst performer during pre-election years.

However, the chart also shows how strong the months that follow can be. We are optimistic that stocks are simply working off the huge start to 2023 and will move to new highs before the year is out.

- September can be a rough month for stocks, but it doesn’t have to be bad.

- Strong wage growth and lower inflation have helped the economy stay resilient.

- The U.S. private sector is the largest holder of U.S. government debt, and thus the biggest beneficiary of higher rates.

- China’s relative holdings of U.S. Treasuries have fallen over the last decade.

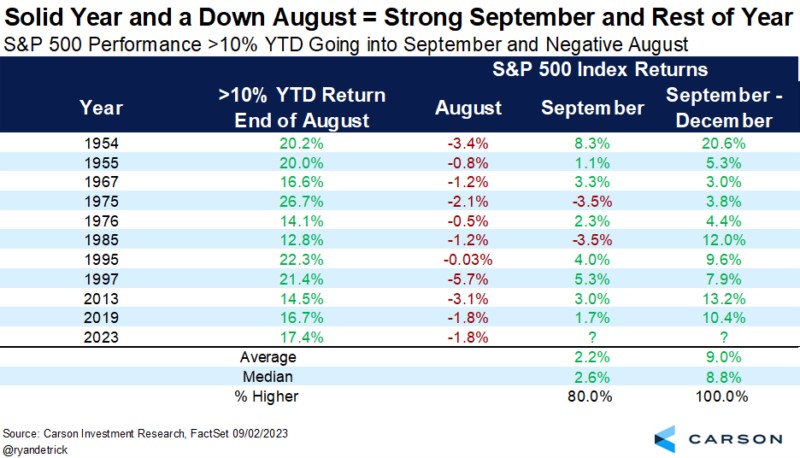

Does September always have to be bad? That’s a common question, especially considering stocks lost 9.3% in 2022 during a horrible bear market and 4.8% in 2021 during a great bull market. To most investors it might feel like September is doomed, but it is not.

Examining previous years that were lower in August but up more than 10% heading into September shows that stocks closed higher eight out of 10 times. Importantly, the rest of the year was higher every time.

Why Has the Economy Stayed Resilient?

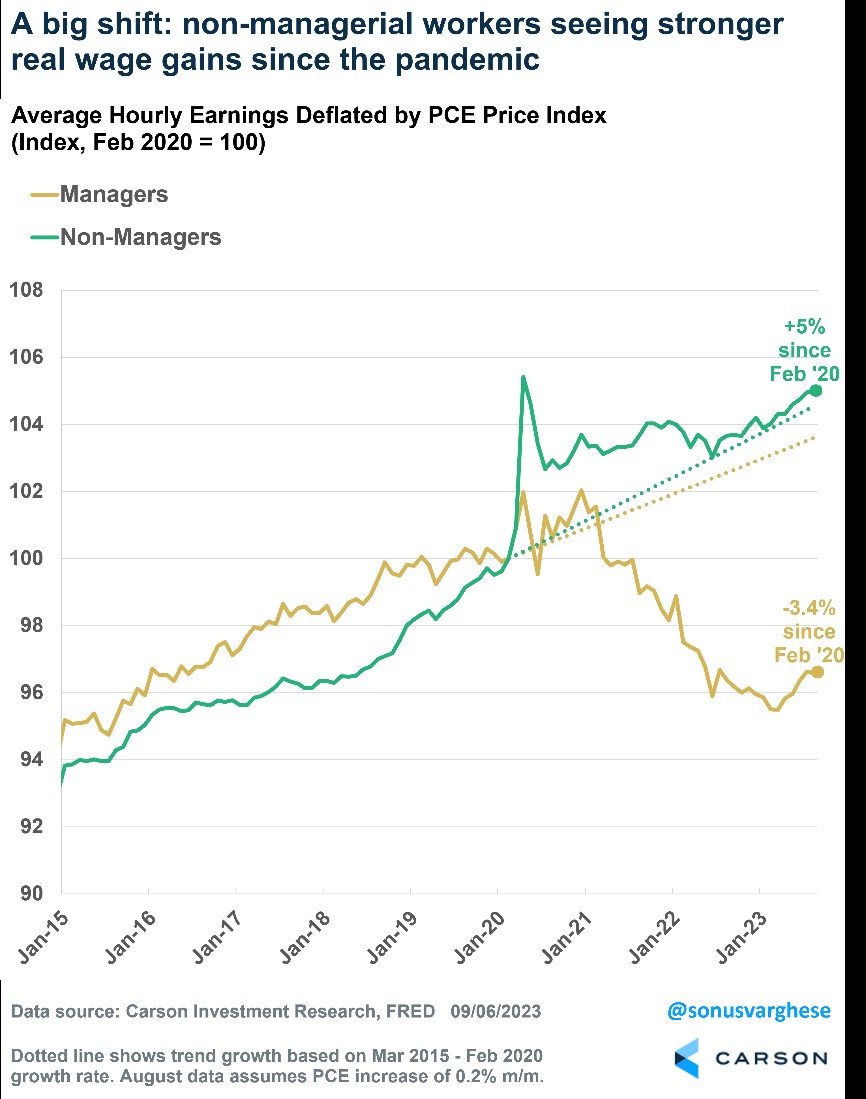

A large part of the economy’s resilience has to do with a strong labor market that has surprised many economists and market-watchers. While employment is certainly slowing from its torrid pace earlier this year, that is likely normalization. Real incomes are rising once again as inflation recedes. But here’s a point not widely talked about: Income growth, especially after adjusting for prices, has been much stronger for “production and non-supervisory” workers, i.e., non-managers, than for managers.

Over the five years prior to the pandemic, inflation-adjusted average hourly earnings for managers grew at an annual pace of 1%. Real income growth for non-managers grew slightly faster, running at a 1.3% annual pace. A stark shift has occurred since the pandemic. Real incomes for non-managers have grown 5% since February 2020 (through August 2023), translating to an annual pace of 1.4%, which is slightly higher than the pre-pandemic trend. However, real incomes have fallen more than 3% for managers. Here’s the non-inflation-adjusted data, since February 2020:

- Average hourly earnings for managers rose 11%.

- Average hourly earnings for non-managers rose 20.7%.

- Prices, as measured by the PCE price index, rose 15%.

Non-managers make up about 81% of private workers and tend to spend a relatively larger portion of their income. That has helped the economy stay resilient and, in fact, grow faster over the past year than it did on average between 2010 and 2019.

Who Holds U.S. Government Debt?

The U.S. government has about $32 trillion in outstanding debt. Surging interest rates have sent interest payments vertical. Interest payments hit 3.6% of GDP in the second quarter of 2023, up from 2.6% before the pandemic and above the historical average of 3.1% (1947-2022). That’s a massive liability for the government. However, the owners of that debt are benefiting though higher interest payments.

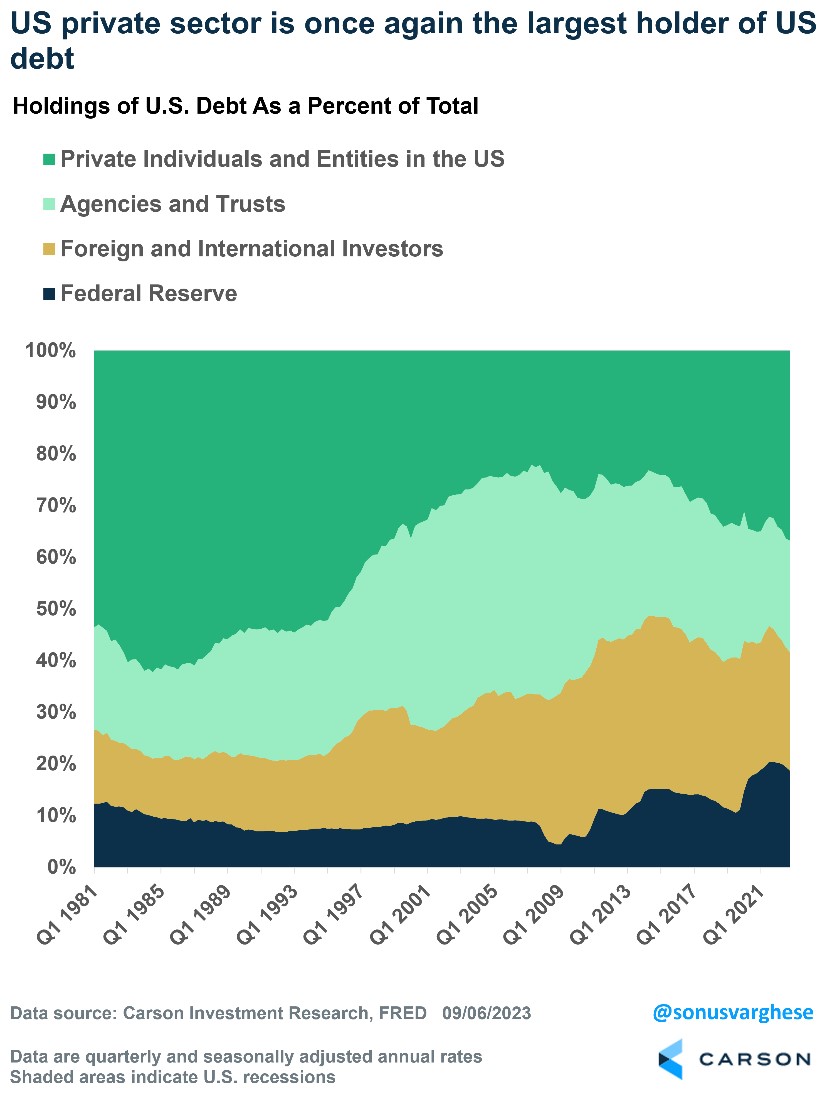

As of the fourth quarter of 2022, the major holders of U.S. debt are:

- The Federal Reserve: $5.9 trillion (19%)

- Foreigners (centrals banks and others): $7.3 trillion (23%)

- Agencies and trusts (Social Security trust fund, etc.): $6.9 trillion (22%)

- Private individuals and entities in the U.S. (households, mutual funds, etc.): $11.7 trillion (37%)

This is a big shift from 2014, when foreigners were the largest holders of U.S. debt, while the U.S. private sector held less than a quarter. The share held by the Federal Reserve has jumped between 2014 and 2022, but the chart below shows that percentage has fallen over the last year as the Fed has ended its bond purchases. The U.S. private sector now holds the largest share of government debt since the late 1990s. The share held by foreigners peaked at just over 33% in 2014 and has been pulling back since.

That means most of the interest payments made by the government are going into the hands of the U.S. private sector. We wouldn’t call this “stimulus,” since people buying Treasuries are unlikely to go out and spend all that extra income. But it’s safe to say, savers in America aren’t complaining about low rates anymore.

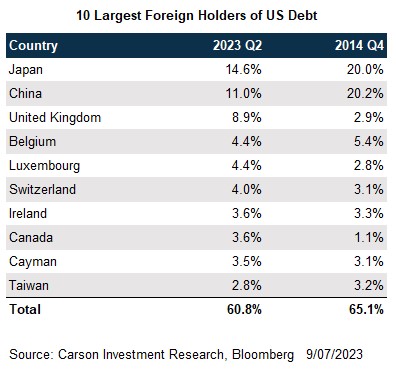

Can China Sell Treasuries and “Hurt” the U.S.?

Foreign holdings of U.S. debt have fallen to less than a quarter of the total. Japan remains the largest holder of U.S. debt. China’s share has fallen. At the end of 2014, China held about a fifth of the foreign share. That’s fallen to 11% as of the second quarter of 2023. It’s also likely China spreads out the source of its purchases of U.S. Treasuries globally, notably using a Belgian custodian for a portion of its holdings — there’s a reason tiny Belgium is the fourth-largest foreign holder of U.S. debt.

Even if all of Belgium’s holdings are attributed to the Chinese, China’s share of foreign U.S. debt has fallen from 26% to 15% between 2014 and 2023. And that is a smaller share of a smaller pie. As a percentage of overall U.S. debt, China’s share has fallen from about 9% to 4%. A primary reason for this decline is that since 2014 China has had to use some of its massive war chest of “foreign exchange reserves,” of which Treasuries are a significant component, to fight capital flight and currency declines amid a weakening economy.

China has different ways of poking the U.S. economy, although many of its methods, including the recent announcement that government officials can’t use Apple phones, are largely for show. But even one of its most powerful levers, which is selling Treasuries, has not had an outsized impact, primarily out of self-interest. Many market participants hardly noticed. (See our recent blog, “Eight Questions About China,” for more on what’s going on in China’s economy.)

—

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case # 01897809-091123_C_T