In the end, stocks had a solid gain in the first quarter. The S&P 500 Index climbed 7.5%, including dividends. But it sure wasn’t easy. After being up more than 8% for the year in mid-February, stocks pulled back sharply, due in part to the banking crisis that took place the second week of March. We continue to believe the economy is strong. Meanwhile, the banking crisis appears to be fading and isolated to a few companies that made some very poor decisions.

- Stocks had a strong first quarter, even though the path wasn’t easy.

- Expect more volatility ahead as sentiment is at a historic low.

- There are positives, including a Fed that may be done with rate hikes, lower inflation, a rebound in manufacturing, and a strong labor market.

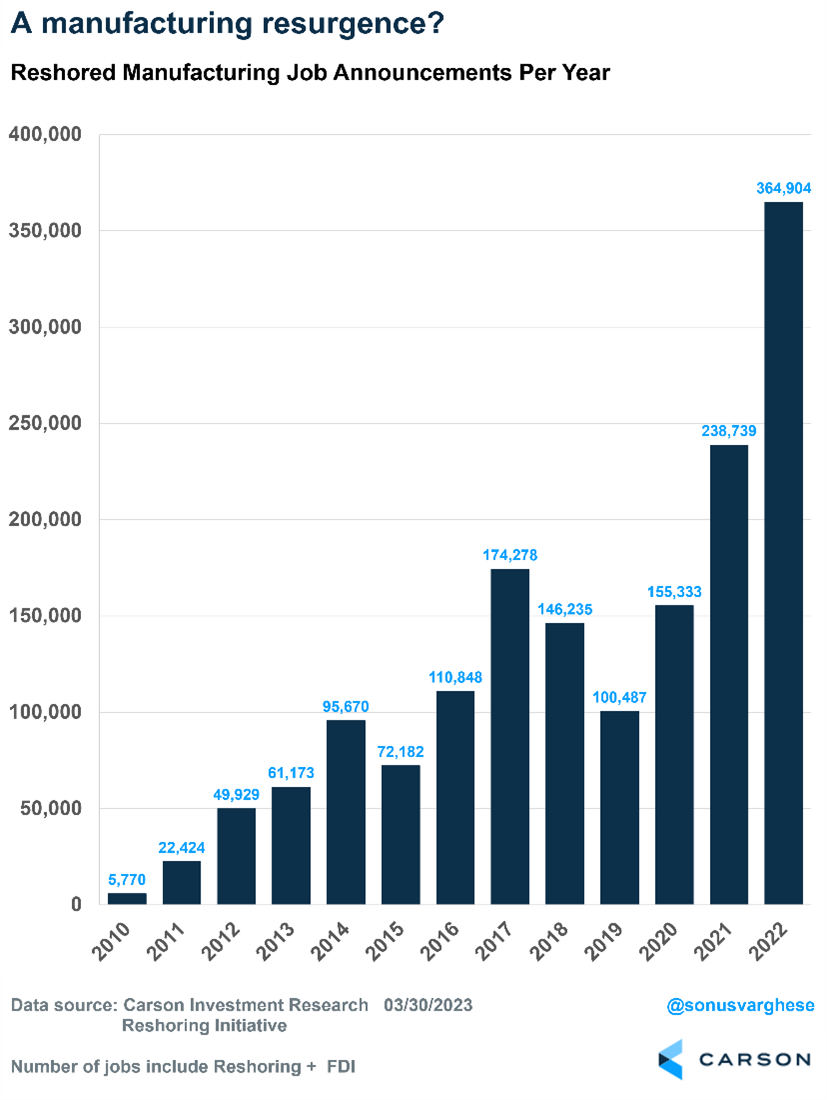

- U.S. companies are re-shoring a record number of manufacturing jobs.

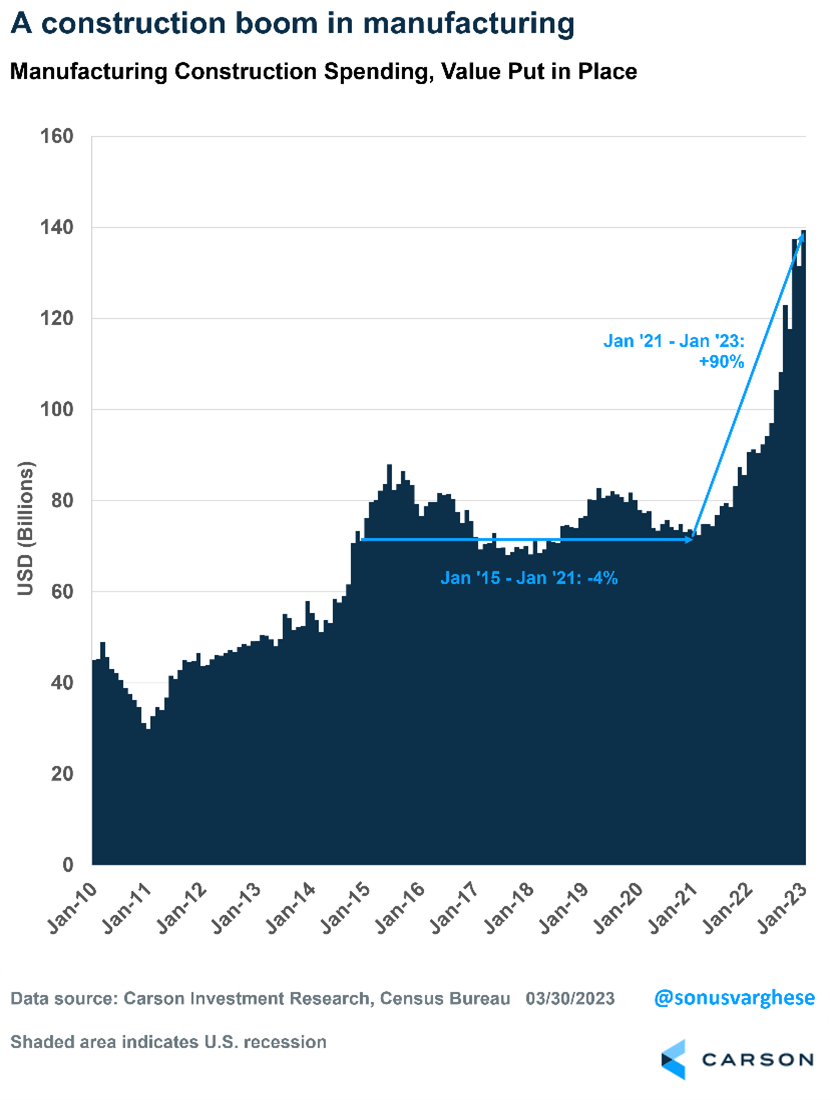

- Manufacturing construction, particularly in the computers and electronics industry, is booming as U.S. industrial policy seeks to promote investment in the sector.

Looking forward in 2023, volatility likely will remain. Overall market sentiment is historically low, and while investors have been concerned about a recession for more than a year, the economy continues to surprise to the upside, led by a strong consumer. The masses are often wrong, which suggests that with so many bears out there, the path could remain upward for stocks.

Certainly, there are still concerns. But whether it’s inflation, the banking crisis, a Federal Reserve policy mistake, a global event, or something else that no one sees coming, worries are part of investing. The positives outweigh the negatives. The Fed seems to be nearly done hiking rates, inflation continues to sink, global manufacturing is rebounding, China continues to reopen, and the employment picture remains healthy.

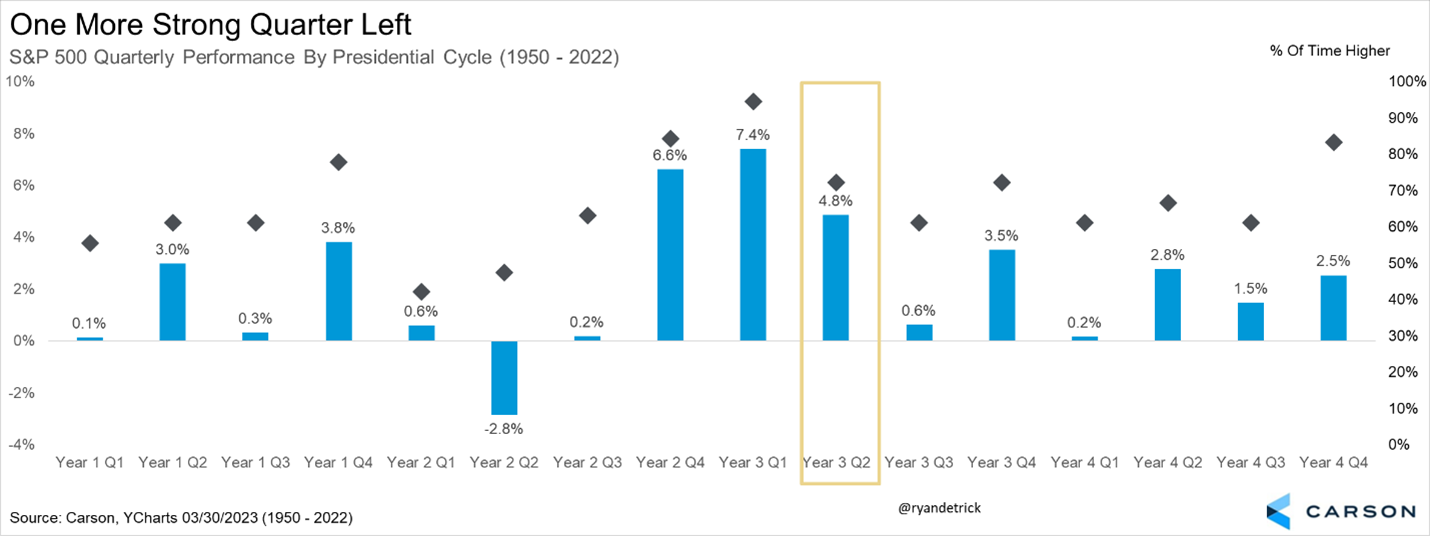

Market performance during the four-year presidential election cycle shows that this quarter is historically quite strong, as are the previous two quarters. The S&P 500 Index added 7.6% in the fourth quarter last year and another 7.5% last quarter, so the trend is playing out well so far. We would never invest blindly based on seasonality, but this could bode well for a continuation of the surprise spring rally.

U.S. Employment Continues to be Strong

The biggest positive going for the economy is employment. Payroll growth has averaged just more than 350,000 over the past three months, and the unemployment rate is 3.6%, close to 50-year lows. Weekly initial claims for unemployment benefits remain low, suggesting employment growth continues to run strong.

Nevertheless, when discussions of the labor market arise, tech sector layoffs loom disproportionately large. This article we wrote puts these layoffs in perspective. The companies making these announcements saw payrolls surge after the pandemic, and now they’re retrenching.

Here’s something else that gets lost in the negative headlines. As good as the labor market is right now, American companies re-shored a record 365,000 manufacturing jobs in 2022. Reported by the Reshoring Initiative, this includes jobs that had previously been held in other countries and jobs created by foreign-owned companies in the U.S.

The 2022 number is a 53% increase from 2021, which itself saw a 54% increase from 2020. These numbers are typically volatile, but the sheer magnitude of the increase suggests the making of a trend.

The report points out that the increase was driven by a surge in electric vehicle batteries and chips, along with a continued uptrend in industries around electrical equipment, chemicals, transportation equipment, and medical equipment.

The increase from 2020-2022 was partly due to companies recognizing that supply chains extending across the world are vulnerable to disruptions and geopolitical events.

The other reason is manufacturing investment in the U.S. is surging after Congress and the president passed last year’s Inflation Reduction Act (IRA) and the Chips and Science Act. We wrote at the time that the IRA was poorly labeled, but it was a big deal and included:

- Taking a practical, all-of-the-above approach to the energy transition, with money for clean energy as well as nuclear power and the oil and gas industry.

- Tax credits and subsidies for clean energy companies, with even traditional infrastructure companies, such as midstream pipelines, benefiting.

- Provisions designed to revive U.S. manufacturing and counter China’s dominance, with the U.S. engaging in industrial policy on a scale not seen in decades.

We wrote at the time that this could potentially incentivize investment in technology and increase productivity, which would be good for workers, let alone economic growth and corporate profits.

It’s nice to see that it’s happening on the ground. Electric vehicle batteries were the most active product to be re-shored in 2022!

And there’s even more evidence.

Manufacturing Construction is Booming

The construction industry has clearly taken a hit from the Federal Reserve’s aggressive interest rate hikes. Mortgage rates surged as a result, and that froze homebuying activity. Single-family housing starts collapsed 32% year-over-year in February 2023. Multi-family housing is holding on, but that’s because many units remain under construction and rental demand is high thanks to low housing inventory.

Since the banking crisis, commercial real estate has come under the microscope. Small banks make a lot of loans to this sector, and a pullback in lending will hurt. But commercial and office construction had already been slowing before the crisis. You just have to walk downtown in any major metro in America to realize that offices are not in great demand.

Yet, here’s what’s interesting, and important.

The total dollar value of all private construction spending rose about $61 billion over the year through January, representing a 4.4% year-over-year increase. Of this, almost $49 billion came from manufacturing construction spending.

As of January, manufacturing construction spending in dollar terms is up 54% year-over-year, and it is up 90% from two years ago.

A year ago (January 2022) manufacturing construction made up about 6.5% of total private construction in the U.S. It’s risen to almost 10% (January 2023).

This is almost entirely driven by the computers and electronics industry and includes investment in semiconductor plants, where construction spending is up 158% year-over-year and a whopping 723% over the last two years!

Construction spending across the rest of the manufacturing industry is up 17% year-over-year. Not too shabby by itself, but it pales in comparison to what’s happening on the computers and electronics side.

Of course, much of this growth is driven by subsidies and tax credits, which are not going to continue year after year. But investment spending tends to feed on itself, especially since it can boost productivity. That’s potentially a huge positive for the U.S. economy over the next decade.

Sometimes it helps to pull back and look at the bigger, longer-term economic picture.

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 – A capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The NASDAQ 100 Index is a stock index of the 100 largest companies by market capitalization traded on NASDAQ Stock Market. The NASDAQ 100 Index includes publicly-traded companies from most sectors in the global economy, the major exception being financial services.

A diversified portfolio does not assure a profit or protect against loss in a declining market.

Compliance Case #01716043